Reduce Your Debt: Effective Tips for Negotiating Collectors

Dealing with debt collectors can be stressful, but understanding your rights and knowing effective negotiation strategies can make a huge difference. Many people avoid calls or feel pressured into paying

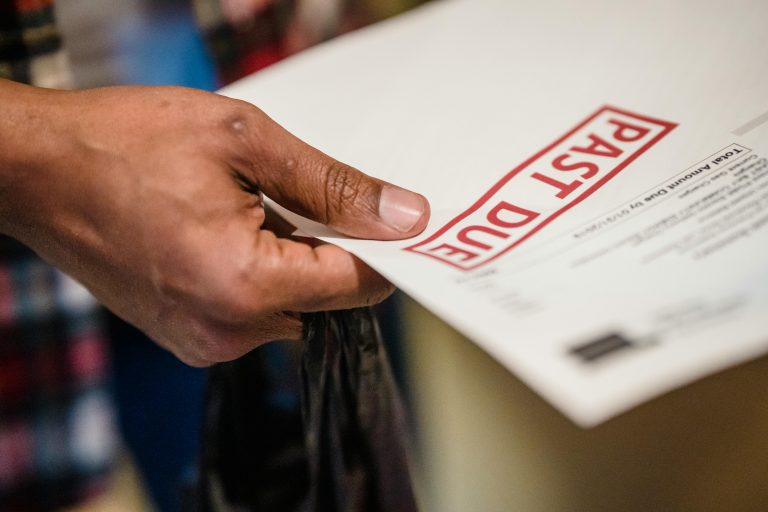

Credit Card Debt Settlement Tips You Can Do Yourself

Struggling with credit card debt can feel overwhelming, but negotiating directly with your creditor is a practical way to reduce your balance and avoid more serious financial consequences. While professional

Benefits of an International Kindergarten Program

Explore the importance and advantages of enrolling children in an international kindergarten program. This long-form article will address common questions and concerns, offering valuable insights for parents considering this educational

What Professionals Look for in Crane Inspection

Crane inspection is a critical aspect of maintaining safety and operational efficiency on construction sites, industrial settings, and other environments where cranes are used. Professionals who perform crane inspections play

10 Medical Career Pathways to Take in 2025

The landscape of medicine is ever-evolving, and as we look towards 2025, it’s important to consider the emerging opportunities that exist across various medical career pathways. Medical professionals of the

Heres What Kind of Flooring Education Institutions Use

Introduction Understanding the types of flooring education institutions use can help policymakers, designers, and administrators make informed decisions. This article explores the most common flooring options, their benefits, and considerations

Discover Curriculum Development Companies Being Used in Modern Schools

Education is an ever-evolving field shaped by a multitude of influences ranging from technological advancements to evolving pedagogical theories. At the heart of this transformation are the curriculum development companies

Essential Services for Professionals From Orthodontics to Angel Investment

Professionals across various industries often require a range of essential services that can enhance both their personal and professional lives. From orthodontic treatment to angel investment opportunities, these services play

Steps to Becoming a Successful Process Server A Comprehensive Guide

Becoming a process server can be a rewarding career choice for those interested in the legal field and with strong organizational and communication skills. A process server plays a crucial

10 Great Trade Career Goals After High School

In today’s world, students are often pressured to pursue traditional college paths after high school. However, there are many alternative career options that do not require a college degree. In this article, we will explore various vocational trades such as roofing, construction, landscaping, flooring, painting, electrical work, mechanic work, woodworking, septic tanks, and plumbing. These